How to Save Money on Blood Glucose Test Strips

Learn how to buy blood glucose test strips online, maximize savings with FSA benefits, and make smart choices to reduce your healthcare expenses.

29 January 2024

For health professionals

![]()

Learn how to buy blood glucose test strips online, maximize savings with FSA benefits, and make smart choices to reduce your healthcare expenses.

We all know that testing your blood sugar accurately and regularly is the most important thing you can do to manage type 1 or type 2 diabetes,1 but health care costs for people with diabetes can add up quickly.

Here are some ways to help lower your day-to-day costs and still get the quality care you need and deserve.

Did you know that medical costs for people with diabetes are more than twice as high as for people without diabetes? In fact:

A survey conducted by Wakefield Research of 500 U.S. adults, ages 26-64, with diabetes and 500 U.S. adults, ages 26-64, without diabetes revealed: 4

Given these challenges, what can you do if you find yourself tempted to cut back on your diabetes self-care? Here are seven ideas that might help:

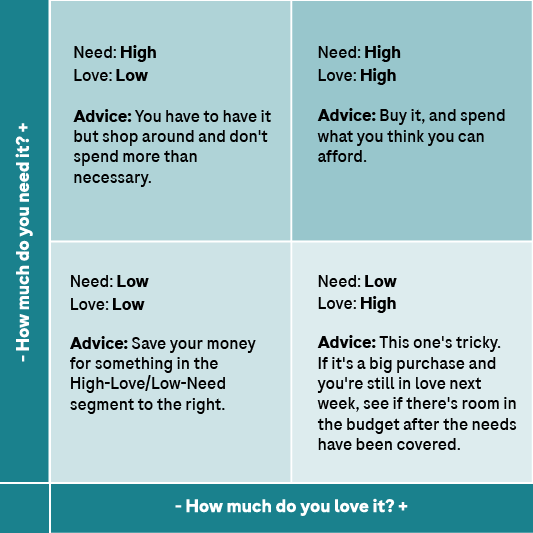

Utilize the “needs vs. wants” matrix. Consider the importance of potential expenditures and decide where something should be on your priority list. Once you've mastered the matrix for cash flow, you can use it for time management, too. We’ve provided an example of one below.

As mentioned above, chasing online deals for test strips can be a hassle, and more often than not the end result isn’t worth the chase– there might be hidden fees or the product itself arrives and isn’t what you thought it was. When it comes to diabetes testing, though, results matter. Here are features to look at no matter where you buy to ensure you’re not falling for a scam.

Buying online isn’t the only way to save. If you have a Flexible Spending Account (FSA), you might already enjoy the savings on meters, lancing devices, test strips and accessories.

Health FSAs are employer-established benefit plans that allow you to pull dollars from your paycheck, pre-tax, to pay for health care costs, like deductibles, copayments, coinsurance, and some drugs. Depending on how much you contribute, it can actually save you money on out-of-pocket family care expenses every year and lower your taxes!7

If you don’t have an FSA yet, here’s everything you need to know about signing up, contributing to your account and spending your FSA dollars on healthcare expenses.

The first step to saving on your health is finding out if you’re eligible. The good news is that more than half of employers offer a flexible spending account (FSA) for their employees 8, so there is a good chance that you have the option available to you – you might be eligible even if you don’t have health insurance.

Most providers let you sign up for an account at the beginning of the calendar year. All you need to do is submit some basic personal information, and you’re on your way to savings. Contact your employer for more detailed information on your company's FSA, including how to enroll.

When you sign up for an FSA, you’ll determine how much to deduct from your paychecks. FSAs use pre-tax dollars, so you won’t have to pay taxes on however much you contribute to your account. Your employer can also contribute to your FSA, but they aren’t required to do so.7

Each year the IRS sets a limit for how much you’re allowed to contribute. In 2026, that amount is $3,400 – which is about $100 dollars more than it was in 2025.9 If you maximize your contributions, that’s roughly $283 each month that you can set aside for healthcare expenses.

If you pay for an eligible expense out of pocket, you can reimburse yourself with your FSA. Save your receipt and submit it through your provider’s online portal. Money will be moved from your FSA back into your pocket.

Even simpler, your provider might offer an FSA card. FSA cards are basically debit cards that are tied to your account. When you go to pay for eligible services or products, you can pay for it directly with your card. No need to worry about reimbursement! Ask your employer or provider for specific details on reimbursement and use of funds.

Unlike other savings accounts like 401(k)s and IRAs, the money you put in an FSA doesn’t roll over into the new year. That means that you’ll need to use all of the money that you’ve contributed this year or you’ll lose it, so try not to contribute more money than you’ll need to cover out-of-pocket health costs for the year.

There are a couple exceptions to this rule, but it is dependent upon your employer as to whether they can be applied to your account or not. For example, you might be granted an extra 2 1⁄2 months to use your FSA dollars from the previous year, or you might be able to roll over up to $680 in 2027.9 Check with your employer to see if they offer either exception.

Since your FSA dollars don’t roll over, you’ll want to spend them before you lose them. Thankfully, there are a number of eligible medical, dental and vision expenses for you to consider.

Your FSA can cover a range of expenses, from routine doctor’s visits to seasonal needs like allergy products or sunscreen.7 You can use it to pay for small expenses like bandages or larger expenses like new eyeglasses and home testing kits. Your spouse’s and child’s expenses are covered, too! If you’re interested in enrolling in a FSA, check with your employer for details on eligible expenses and claim procedures.

Here are just a few diabetes care items that can help you use your FSA dollars before they expire:

Footnotes

Accu-Chek Newsletter

Get diabetes management tips and news delivered right to your inbox.